Quick Facts

- Market Reaction: On January 30, 2026, the S&P 500 closed down 0.43% and the Nasdaq Composite fell 0.94% in immediate response to the transition news.

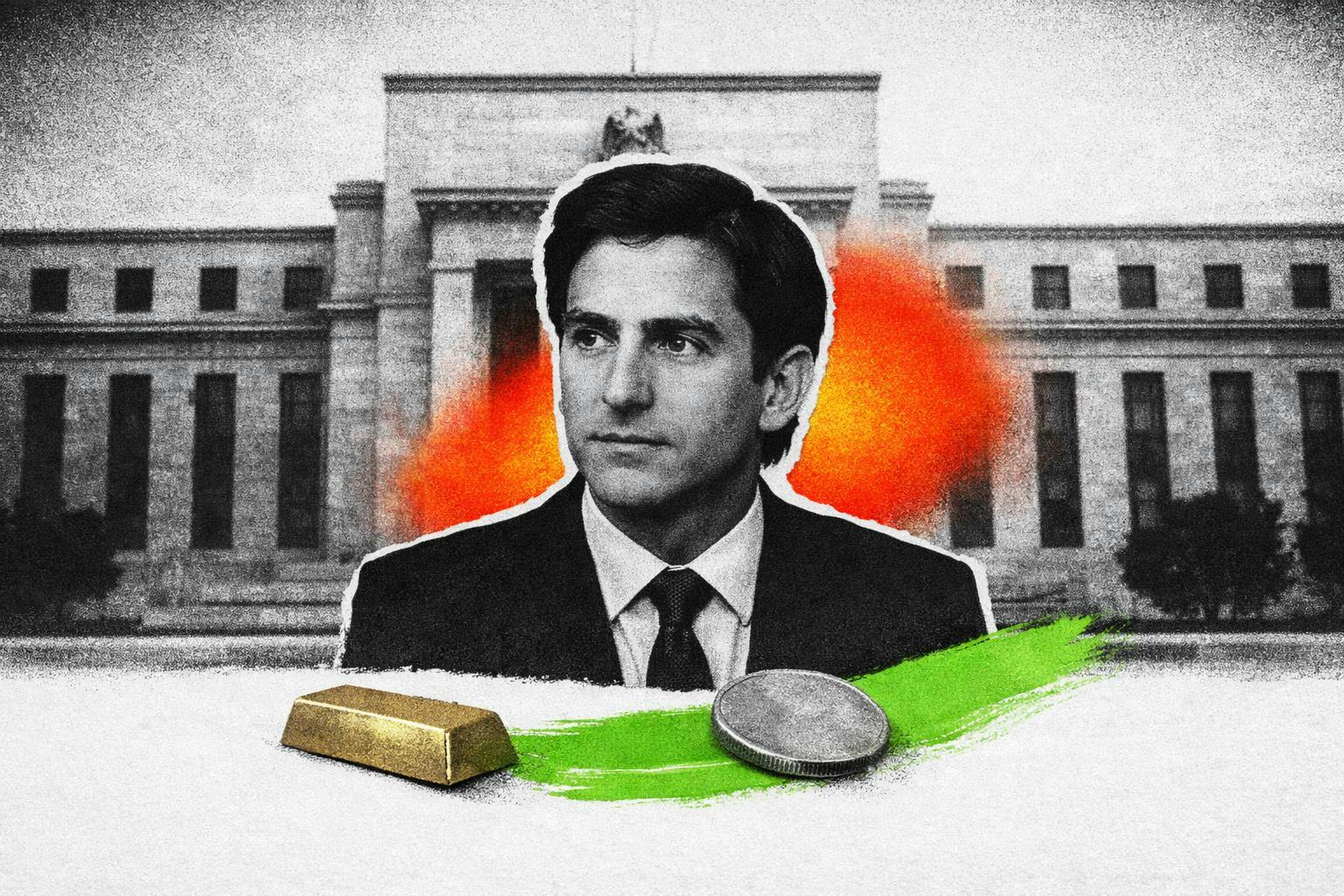

- The Nominee: Kevin Warsh, recognized for advocating a rules-based policy framework and a leaner central bank footprint.

- Macro Catalyst: The announcement coincided with December Core Producer Price Index data reaching 0.7%, significantly higher than the 0.2% forecast.

- Yield Thresholds: The 30-year Treasury yields surged past the 5% mark as investors priced in a more aggressive hawkish monetary policy impact.

- Historical Context: Market data suggests that indices often face an average correction of 14% during the initial six months of a new Federal Reserve chair’s term.

- Balance Sheet Outlook: UBS strategists estimate that a rapid reduction of the $7 trillion balance sheet could create a 9-percentage-point headwind for the S&P 500 over the next three years.

The announcement of a new Fed chair nomination on January 30, 2026, sent shockwaves through Wall Street, with the Nasdaq falling nearly 1% as investors braced for a hawkish transition. By combining a shift in FOMC leadership with unexpected inflationary signals, the market signaled a major risk-off sentiment. The stock market sell-off following the Fed chair nomination was primarily driven by the nominee’s reputation as a monetary hawk. Investors anticipate that a hawkish leadership shift will prioritize inflation control and a reduction of the Federal Reserve’s balance sheet over accommodative policy. This outlook suggests that interest rates may remain higher for longer, increasing borrowing costs and strengthening the US dollar, which typically pressures equity valuations.

| Policy Feature | Jerome Powell (Adaptive) | Kevin Warsh (Rules-Based) |

|---|---|---|

| Primary Philosophy | Data-dependence and discretionary adjustment | Adherence to fixed economic rules and price stability |

| Forward Guidance | Highly telegraphed and transparent | Potential reduction in "pre-stated" market signals |

| Market Support | Active use of the "Fed Put" during volatility | Preference for market-driven corrections and discipline |

| Balance Sheet | Gradual quantitative tightening | Accelerated reduction of the Fed's $7 trillion portfolio |

| Inflation Target | Flexible 2% average targeting | Strict focus on curbing inflationary momentum |

Reason 1: The 'Hawk' Signal and a Shift to Rules-Based Policy

The primary catalyst for the recent market volatility is the perceived end of the adaptive era. For years, investors grew accustomed to a Federal Reserve that was data-dependent, often stepping in with accommodative measures when market turbulence threatened the broader economy. The Fed chair nomination represents a move toward a rules-based policy framework. This philosophy suggests that the central bank will move away from discretionary interventions and instead follow a more predictable—yet rigid—mathematical approach to setting interest rates and managing the money supply.

While predictability sounds positive, the immediate impact on equity markets is the removal of the Fed Put. This long-standing psychological cushion gave investors confidence that the central bank would provide liquidity during downturns. Under a hawkish leadership, that support is no longer guaranteed. For tech stock risks during hawkish fed chair transition, this is particularly punishing. High-growth companies that rely on cheap capital to fund expansion are finding their safety nets pulled away. The nominee’s history on the Federal Reserve board during the 2008 crisis further solidifies the view that he favors central bank independence and less intervention, leading to a structural headwind for equity valuations that had been inflated by years of liquidity.

Reason 2: The Inflationary 'Double-Whammy' of PPI Data

Market participants rarely react to a personnel change in a vacuum. The timing of the Fed chair nomination was critical, occurring alongside the release of the Producer Price Index data. When the core PPI surged to 0.7% in December, nearly triple the expected figure, it confirmed the market's worst fears: inflation is prove more "sticky" than previously hoped. This creates a transmission mechanism where high wholesale prices force a hawkish chair to act even more aggressively than they might in a low-inflation environment.

The combination of a hawkish nominee and hot inflation data creates an environment where quantitative tightening is expected to accelerate. As the Federal Reserve moves to shrink its balance sheet, the amount of cash circulating in the financial system decreases. This typically results in a stronger ICE US Dollar Index, which is often a negative indicator for multinational corporations. When the dollar is strong, international earnings are worth less when repatriated, and American products become more expensive for global buyers. This inflationary double-whammy has forced many participants to adopt an investment strategy interest rate hikes require, shifting away from global growth and toward domestic defensive plays.

Reason 3: The Death of 'Forward Guidance' and Higher Volatility

For nearly a decade, the Federal Reserve has utilized forward guidance to "telegraph" its moves months in advance. This transparency was designed to minimize market shocks. However, the new nomination signals a potential return to an era where the central bank does not feel obligated to signal every single basis point move. This increase in uncertainty is a primary driver of risk-off sentiment. If the FOMC leadership transition includes a departure from telegraphed decisions, investors must include a larger "uncertainty premium" in their models.

This shift directly impacts discounted cash flow valuations. In a world where the Treasury yield curve is steepening and the 30-year bond has jumped above 5%, the present value of future earnings for growth stocks is drastically reduced. We are seeing a shift from risk-on assets into short-duration bonds and value stocks that generate cash flow today, rather than a decade from now. This is a classic bear steepener scenario, where long-term rates rise faster than short-term rates, signaling that while the market expects growth, it also expects the cost of that growth to be significantly higher under a new leadership regime.

Navigating the Shift: Strategy for Investors

When facing a hawkish transition, the most important task for an investor is rebalancing. History tells us that during these shifts, a growth vs value rotation is almost inevitable. Capital moves from higher-multiple sectors like technology and consumer discretionary into areas that provide a natural hedge against rising interest rates.

Identifying the Winners and Losers

- Financials (Banks & Insurance): These are often the primary beneficiaries. A steeper treasury yield curve allows banks to lend at higher long-term rates while paying out less on short-term deposits, expanding their net interest margins.

- Energy and Materials: These sectors often serve as a hedge when Producer Price Index data is high, as the value of the underlying commodities tends to rise with inflation.

- Healthcare and Consumer Staples: These are traditional defensive stock sectors for hawkish monetary policy. People still need medicine and groceries regardless of whether the Fed chair is a hawk or a dove.

- The Losers (Tech & Real Estate): Interest rate sensitive stocks are the first to be sold off. Real Estate Investment Trusts (REITs) struggle with higher borrowing costs, while "Big Tech" faces multiple compression as the risk-free rate (treasury yields) increases.

Portfolio Tactics

Investors should consider how to adjust portfolio for kevin warsh nomination by looking at bond durations. With a hawkish Fed, long-term bonds are prone to price drops as yields rise. Shifting toward a bond market and treasury yield strategy under kevin warsh might involve shortening duration—moving into 2-year or 5-year notes—or looking at inflation-protected securities (TIPS).

Furthermore, hedging stock market risk during fed chair confirmation is a prudent move for those with heavy equity exposure. This can be achieved through interest rate futures or by increasing cash positions to wait for a more stable entry point once the Senate Banking Committee finishes the confirmation process. Rebalancing rate sensitive stocks after fed chair pick is not about exiting the market entirely; it is about ensuring that your portfolio is not overly exposed to the sectors that current Fed rhetoric is actively cooling down.

FAQ

Who nominates the Federal Reserve Chair?

The President of the United States has the constitutional authority to nominate the Chair of the Board of Governors of the Federal Reserve System. This choice is often based on the nominee’s economic philosophy and their ability to maintain the central bank independence while pursuing the dual mandate of price stability and maximum employment.

What is the confirmation process for a Fed Chair nominee?

Once the President makes a formal nomination, the individual must undergo a rigorous vetting process. This includes financial disclosures and background checks, followed by public hearings where the nominee is questioned on their economic outlook and proposed policy framework.

Does the Senate have to approve the Fed Chair nomination?

Yes, the nomination requires a simple majority vote for approval in the United States Senate. The Senate serves as a check on executive power, ensuring that the nominee possesses the necessary qualifications and temperament to lead the world's most influential central bank.

What is the role of the Senate Banking Committee in the nomination?

The Senate Banking Committee is the first hurdle in the confirmation process. They conduct the initial hearings and vote on whether to send the nomination to the full Senate floor. The committee’s endorsement is a critical signal of the nominee’s likelihood of being confirmed.

What happens if the Fed Chair nominee is not confirmed?

If the Senate rejects a nominee, or if the nominee withdraws their name due to opposition, the President must select a new candidate. In the interim, the Vice Chair of the Federal Reserve usually serves as the acting leader to ensure there is no vacuum in central bank leadership and to maintain continuity in monetary policy.