Quick Facts

- Market Context: Homeowners in the United States reached a record $11.5 trillion in tappable equity as of the second quarter of 2024, representing a 9.2% increase from the previous year.

- The Strategy: Retirees can maximize home equity retirement income by combining a Home Equity Conversion Mortgage (HECM) with a Qualified Longevity Annuity Contract (QLAC).

- Accessible Wealth: The average mortgage holder has roughly $214,000 in accessible equity while maintaining a 20% safety cushion.

- Longevity Buffer: A HECM provides tax-free liquidity in early retirement, while a QLAC generates guaranteed lifetime cash flow starting at age 85.

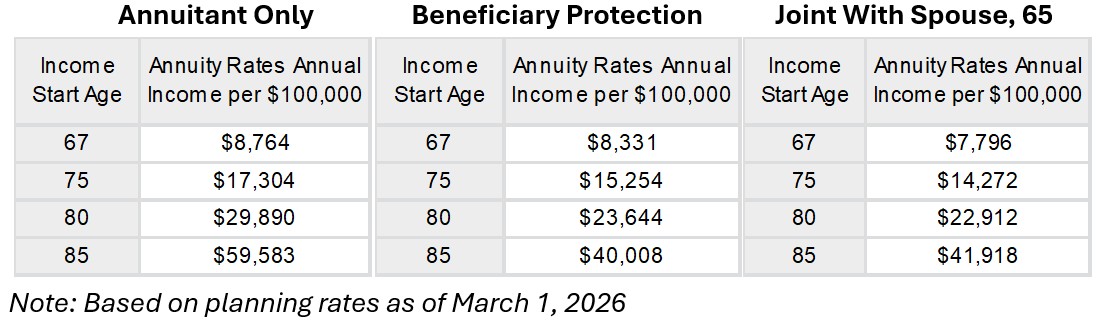

- Tax Advantages: Utilizing a QLAC allows retirees to defer taxes on up to $210,000 of a rollover IRA, reducing Required Minimum Distributions.

- Net Worth Gap: Homeowner median net worth is $396,200, which is nearly 40 times higher than the median net worth of renters.

As Social Security faces potential cuts by 2033, retirees are looking for stable home equity retirement income. By leveraging a HECM and QLAC strategy, you can unlock housing wealth for longevity protection and bridge the gap between traditional savings and lifetime financial security.

The 2033 Social Security Risk: Why Housing Wealth is the New 'Fourth Leg'

For decades, retirement planning was built on a three-legged stool: Social Security, employer-sponsored pensions, and personal savings. However, with the Social Security Administration projecting a 23% benefit cut by 2033 if the trust fund is depleted, that stool is looking increasingly unstable. For the modern retiree, housing wealth longevity protection has moved from a backup plan to an essential fourth leg of the retirement pillar.

The traditional mindset often viewed home equity as a last resort, something to be touched only in a dire emergency. But the financial landscape has shifted. We are seeing a generation of retirees who are asset-rich but income-poor. While they may have hundreds of thousands of dollars locked in their primary residence, their monthly cash flow from traditional portfolios is vulnerable to market volatility protection needs. By rebalancing assets to include home equity, retirees can mitigate sequence of returns risk—the danger of a market downturn early in retirement forcing the sale of stocks at a loss.

Legislation like the SECURE Act and SECURE 2.0 has further incentivized this shift. These laws have modernized the rules around retirement accounts, making it easier to utilize a deferred income annuity combined with HECM line of credit to manage long-term risks. Instead of watching a portfolio dwindle, retirees can use their home to provide a non-recourse volatility protection buffer that keeps their other investments intact during lean years.

The HECM and QLAC Strategy: A Masterclass in Laddered Protection

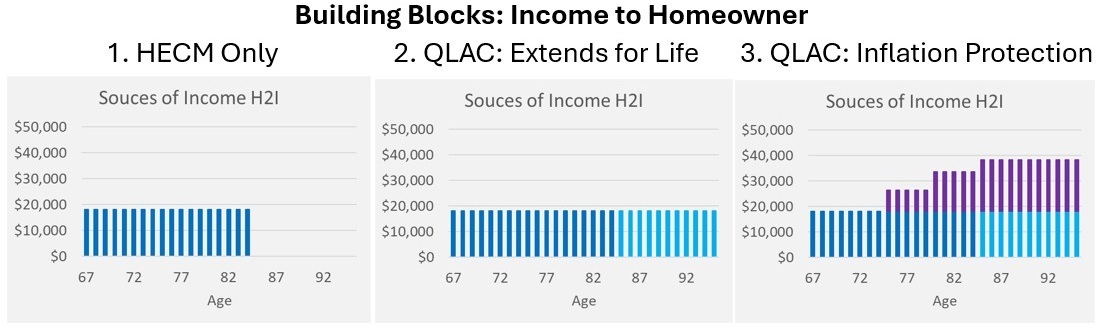

To truly turn a home into a lifetime income stream, a sophisticated HECM and QLAC strategy for retirement is often the most effective approach. This strategy creates a "ladder" of income. In the first phase of retirement, typically from age 62 to 85, the homeowner uses a Home Equity Conversion Mortgage. This FHA-insured loan allows you to access equity without a monthly mortgage payment, though you remain responsible for property taxes and insurance.

The second phase of the strategy involves the Qualified Longevity Annuity Contract. Under current IRS rules, you can move up to $210,000 from a rollover IRA into a QLAC. This money is removed from your Required Minimum Distributions (RMD) calculations, providing immediate tax relief. The QLAC then remains dormant until you reach a specific age, usually 85, at which point it begins paying out a guaranteed monthly check for the rest of your life.

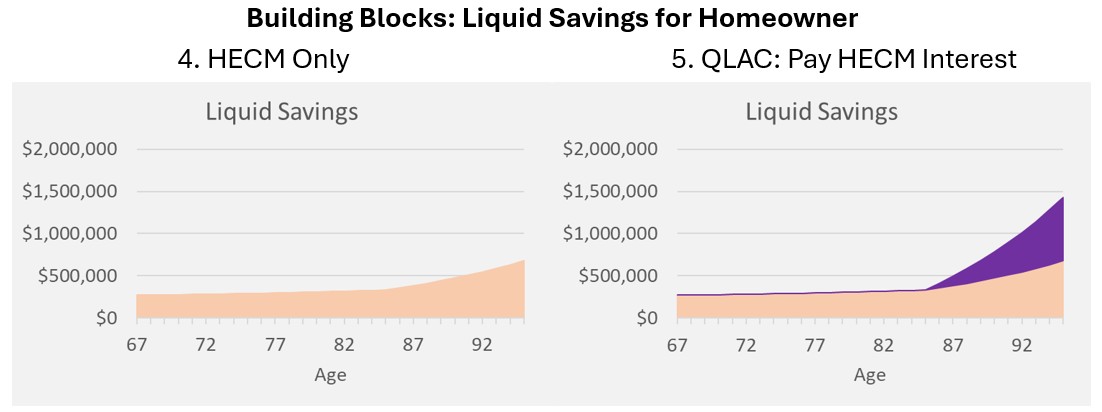

The technical synergy here is powerful. During the early years, the HECM line of credit or tenure payments provide the cash flow needed to maintain a lifestyle or cover healthcare costs. Because this money is technically a loan advance, it is generally considered tax-free. When the retiree turns 85, the QLAC kicks in. These lifetime guaranteed payouts can then be used to pay down the accruing interest on the reverse mortgage for lifetime income, effectively preserving the remaining credit line for heirs or emergency long-term care needs. This creates a cycle of tax-advantaged withdrawal that protects the primary portfolio from depletion.

Accessing Equity without Debt: Home Equity Investments (HEI) vs. Reverse Mortgages

While a HECM is a popular choice for many, it is not the only way to tap into housing wealth for longevity protection. Some retirees prefer to avoid debt altogether. This is where Home Equity Investments (HEI) come into play. Unlike a reverse mortgage, an HEI is an equity sharing agreement. An investor provides a lump sum of cash today in exchange for a percentage of the home’s future appreciation.

For a retiree with a lower credit score—some HEI providers accept scores as low as 500—this can be an attractive alternative. However, it lacks the FHA-insured loans protections and the flexible payout options of a HECM. To help you decide, consider the following comparison of how to turn home equity into an annuity versus a simple equity share.

| Feature | HECM (Reverse Mortgage) | Home Equity Investment (HEI) |

|---|---|---|

| Monthly Payments | None (Retiree pays taxes/insurance) | None |

| Payout Options | Line of Credit, Tenure, Lump Sum | Lump Sum only |

| Repayment | When home is sold or last borrower leaves | End of term (typically 10-30 years) |

| Ownership | Retiree retains 100% of title | Retiree retains title; Investor shares appreciation |

| Credit Req. | Moderate (Focus on residual income) | Low (Often as low as 500) |

| Protection | Non-recourse feature (FHA insured) | Varies by contract |

Choosing between these products depends heavily on your cash-flow management needs. A HECM offers a line of credit that grows over time, which is a unique hedge against inflation-adjusted payouts. In contrast, an HEI is better suited for a one-time capital influx to fund a specific retirement goal, such as purchasing a smaller property or paying off high-interest debt.

Protecting Your Heir: Debunking the Inheritance Myth

Perhaps the biggest hurdle for retirees considering using home equity for lifetime guaranteed income is the fear of "losing the house" to the bank. This myth often prevents families from utilizing their most significant asset. In reality, modern HECM regulations include a non-recourse feature. This means that neither the borrower nor their heirs will ever owe more than the home’s worth at the time of sale, even if the loan balance exceeds the property value due to market drops.

Furthermore, using home equity assets to fund retirement often leads to a higher estate liquidity. By using the home to provide monthly income, you can avoid selling stocks during a market downturn, allowing your liquid portfolio to continue growing. Financial modeling has shown that for many mass affluent households, a HECM can actually increase the final net worth of an estate—sometimes by as much as $800,000 over a 30-year retirement—simply by preserving the tax-deferred growth of an IRA or 401(k).

Protecting surviving spouse with housing wealth strategies is also a critical component. If both spouses are on the HECM loan, the surviving spouse can remain in the home and continue receiving payments or accessing the line of credit even after the first spouse passes away. This continuity prevents a sudden drop in living standards during an already difficult transition.

FAQ

How can I use my home equity for retirement income?

There are several ways to convert your home equity into cash flow. The most common is a HECM, which offers monthly tenure payments, a line of credit, or a lump sum. Alternatively, you can use a Home Equity Investment (HEI) to get a lump sum without monthly interest, or a standard HELOC if you have the income to support monthly interest payments.

Is money received from home equity taxable in retirement?

Generally, no. Because the funds from a HECM or HEI are considered loan proceeds or an equity exchange rather than earned income, they are typically tax-free. This makes housing wealth an excellent way to manage your tax bracket in retirement, especially if you are also taking taxable distributions from a traditional IRA.

What are the pros and cons of a reverse mortgage for retirement income?

The pros include no monthly mortgage payments, the non-recourse feature that protects heirs, and the ability to stay in your home. The cons include the accrual of interest over time which reduces the remaining equity, upfront closing costs, and the requirement to keep up with property taxes, insurance, and maintenance.

Can I use my home equity to pay for long-term care in retirement?

Yes, home equity is a frequent source of funding for in-home care or long-term care insurance premiums. The HECM line of credit is particularly useful for this, as the unused portion of the line grows over time, providing a larger pool of funds as you age and your health needs increase.

Is it better to use a HELOC or a reverse mortgage in retirement?

A traditional HELOC usually requires monthly interest payments and has a limited "draw period," after which you must repay the principal. This can create a cash-flow burden. A reverse mortgage is often better for retirees because it requires no monthly principal or interest payments, making it a more stable choice for those on a fixed income.

Planning Your Housing Wealth Roadmap

Unlocking the value of your home is not a decision to be made in a vacuum. It requires a holistic look at your entire financial picture, from your tax-advantaged withdrawal strategy to your estate goals. For those at least 62 years old living in their primary residence, a HECM and QLAC strategy provides an unmatched level of longevity protection.

Before moving forward, I recommend a three-step checklist:

- Consult a CFP: A certified financial planner can model how a reverse mortgage for lifetime income affects your total portfolio longevity.

- Attend HECM Counseling: This is a mandatory FHA requirement that ensures you fully understand the costs and responsibilities of the loan.

- Review Tax Implications: Speak with a tax professional about how QLAC payments and HECM interest might interact to provide potential tax benefits of QLAC and reverse mortgages.

Your home has worked hard for you over the decades, appreciating in value while providing shelter. In this new era of retirement, it is time for that asset to work just as hard at providing the income you need to enjoy your golden years with confidence.