Our Top Picks

- Boldin (formerly NewRetirement): Best for comprehensive scenario modeling, offering deep dives into Roth IRA conversion ladders and 15+ interactive variables.

- MaxiFi: Best for economic-based consumption smoothing, using a unique algorithm to maximize and stabilize your annual spending power.

- Empower: Best free dashboard for high-net-worth investors, providing an automated overview of asset allocation, net worth, and investment fees.

- Origin: Best for AI-driven insights, utilizing natural language processing to integrate budgeting with long-term financial goal tracking.

Savvy DIY investors should select retirement planning software that prioritizes multi-scenario modeling and tax-aware withdrawal logic over simple budget tracking. Choosing the right retirement planning software is critical for savvy DIYers who want to move beyond spreadsheets by leveraging advanced retirement scenario modeling and tax-efficient retirement withdrawals, allowing you to bypass the traditional 1% AUM advisor fee while maintaining professional-grade precision.

The ROI of DIY Financial Planning: Software vs. 1% AUM

For years, the standard path for wealth management was to hand over a 1% annual fee based on assets under management to a professional advisor. On a $1 million portfolio, that translates to $10,000 every single year. In contrast, the current crop of premium retirement planning software costs between $120 and $150 annually. Over a 30-year horizon, the difference in fees alone, when compounded at a modest 7% return, could result in a difference of hundreds of thousands of dollars in your total nest egg.

The shift toward self-directed planning is backed by recent data. According to the Employee Benefit Research Institute, the usage of online retirement calculators among investors increased from 17% in 2000 to 48% in 2020. This trend has only accelerated. A survey of U.S. respondents in 2026 revealed that 60% use online calculators and 55% use retirement apps as their first resource for financial information, compared to only 24% who consult a financial adviser first.

By taking control of their diy financial planning, investors are finding they can leverage professional-grade asset allocation strategy and stochastic modeling without the high overhead. These tools provide the transparency needed to understand exactly how market volatility and fees impact long-term success.

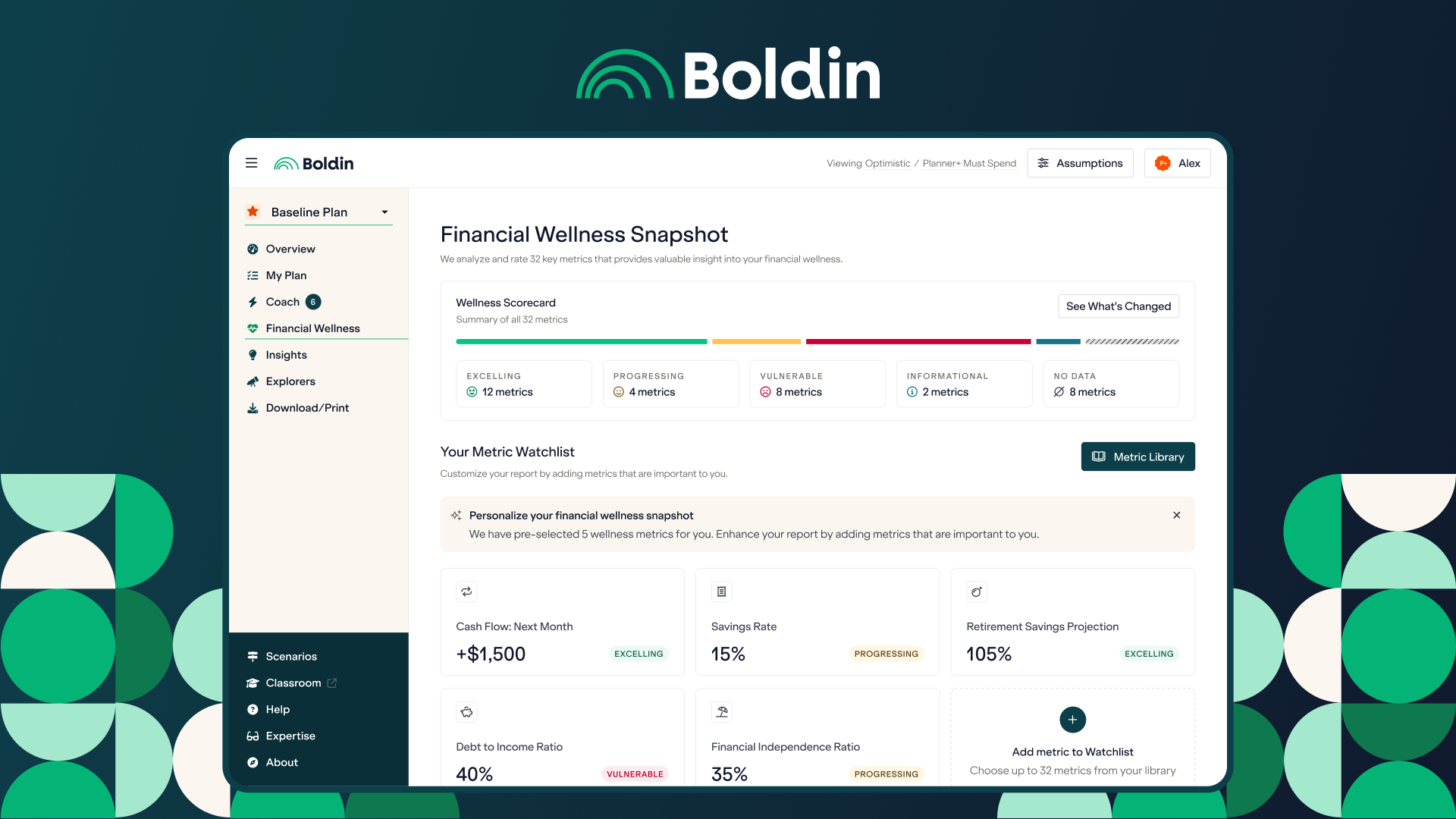

1. Boldin (NewRetirement): Best for Comprehensive Scenario Modeling

Boldin has quickly become the go-to platform for the data-driven investor, or those often referred to as financial data nerds. Managing over $300 billion in assets through its user-directed plans, it excels in allowing users to test an almost infinite number of what-if scenarios. While many tools give you a simple green or red light for success, Boldin allows you to play with more than 15 variables including inflation rates, housing changes, and healthcare costs.

One of the standout features of this retirement planning software is its focus on Roth IRA conversion ladders. For those looking to minimize their lifetime tax bill, Boldin provides a roadmap for moving assets from tax-deferred accounts to tax-free ones during lower-income years. This helps mitigate the impact of Required Minimum Distributions (RMDs) later in life.

The platform relies heavily on probabilistic forecasting to show a range of probable outcomes rather than a single static number. This transparency into the sequence of returns risk helps DIYers understand the impact of a market downturn in the early years of retirement. It is essentially pro-level retirement software for self-directed individual investors who want to understand the mechanics behind their financial plan.

| Feature | Boldin (Paid Version) |

|---|---|

| Best For | Strategic Scenario Planning |

| Cost | ~$120/year |

| Key Capability | Roth Conversion Modeling |

| Modelling Type | Deterministic & Probabilistic |

2. MaxiFi: Best for Economic-Based Consumption Smoothing

MaxiFi takes a fundamentally different approach to retirement planning. While most tools focus on hitting a specific savings target, MaxiFi uses an algorithm designed by economist Laurence Kotlikoff to solve for consumption smoothing. The goal is to maximize your living standard throughout your life, ensuring you don't live too high today at the expense of your future self, or vice versa.

This best financial planning software for individual consumption smoothing ignores the traditional Monte Carlo approach in favor of a stable discretionary spending model. It looks at your assets, projected income, and taxes to tell you exactly how much you can spend this year and every year after. This provides a clear, actionable cash flow forecasting model that many retirees find more intuitive than a percentage chance of success.

For savvy DIYers, MaxiFi is particularly powerful for Social Security benefit optimization. It runs thousands of calculations to determine the exact month you and your spouse should claim benefits to maximize your lifetime collective income. It is a highly precise tool for those who prioritize a consistent, predictable lifestyle.

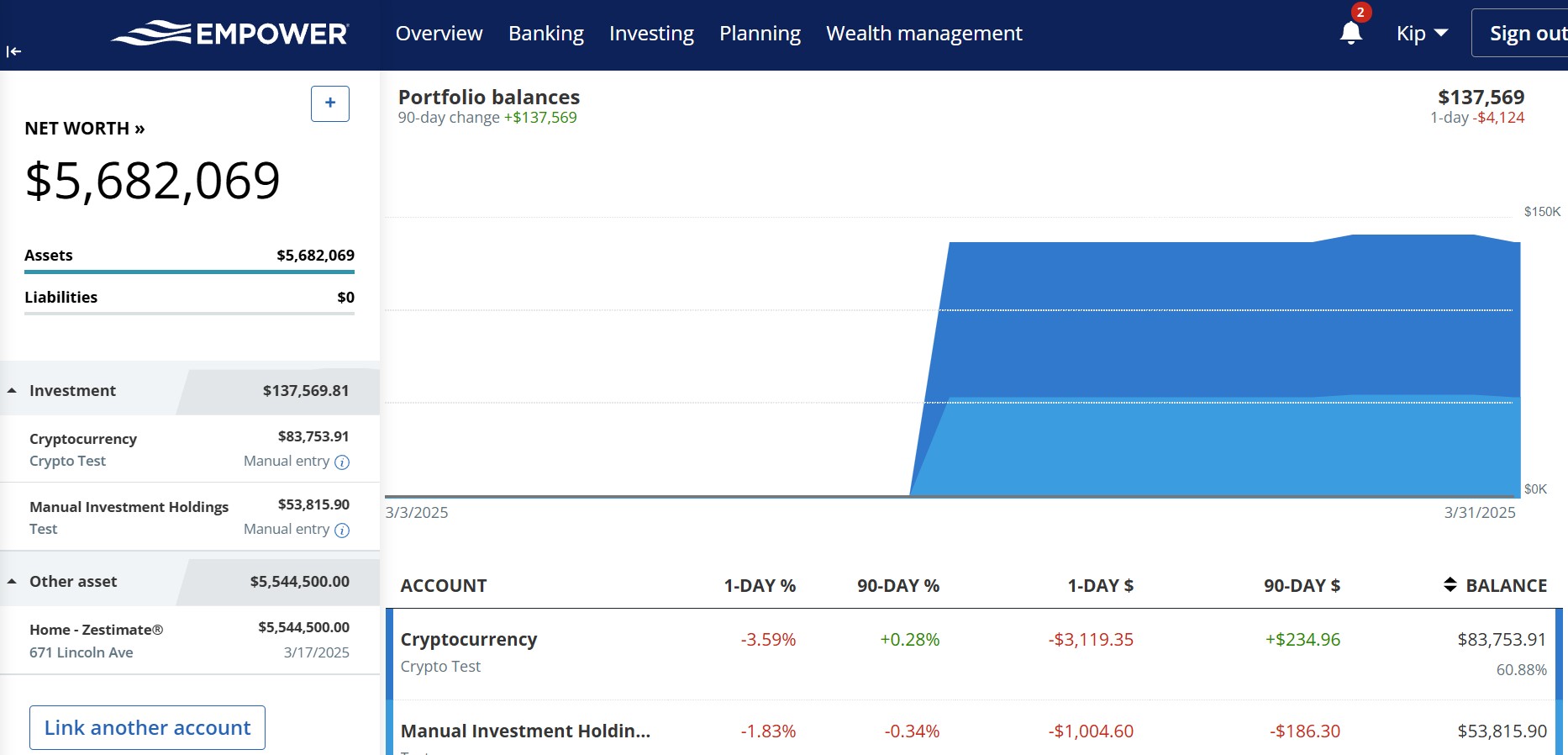

3. Empower: Best Free Dashboard for High-Net-Worth Tracking

If you are looking for a comprehensive overview of your current financial state without a subscription fee, the Empower Personal Dashboard is the industry gold standard. It uses automated account linking to provide a real-time view of your net worth, cash flow, and asset allocation strategy across all your accounts.

The Empower retirement planner is surprisingly robust for a free tool. It is designed to perform 5,000 Monte Carlo simulations to deliver household projections based on variables such as market volatility and tax rules. This allows users to visualize how their current savings rate and investment choices align with their long-term goals.

A major benefit for diy financial planning is the tool's fee analyzer. It scans your 401(k) and brokerage accounts to identify hidden investment fees that could be eroding your returns. While the platform does offer human advisory services for those with significant assets, the free software remains a powerful standalone resource for managing sequence of returns risk and maintaining a balanced portfolio.

4. Origin & ProjectionLab: Best for Privacy and AI-Driven Insights

As we move into 2026, AI-driven financial platforms like Origin are changing how we interact with our money. Origin uses natural language processing to let you ask complex questions about your finances, such as "How much more can I save if I cut my travel budget by 20%?" or "What happens to my retirement age if inflation stays at 4%?" This makes expert-level financial strategy more accessible for self-directed individuals by bridging the gap between raw data and actionable decisions.

For users who are part of the FIRE movement (Financial Independence, Retire Early), privacy and manual control are often more important than automated syncing. ProjectionLab offers a middle ground, allowing for detailed cash flow forecasting without necessarily requiring you to link your bank accounts. It is highly visual and focuses on the journey toward early retirement, making it a favorite for those who want to model extreme saving and withdrawal scenarios.

Both tools represent the modern edge of retirement planning software, focusing on user experience and the integration of daily budgeting with long-term goals.

Strategy Deep Dive: Managing Tax-Efficient Withdrawal Sequencings

The real value of sophisticated retirement tools lies in their ability to handle tax-efficient retirement withdrawals. It is not just about how much you save, but how you take it out. A properly modeled strategy can often increase a household’s spendable wealth by significantly more than simple asset selection alone.

Most high-level tools now model the 27% wealth increase possible from shifting from a basic withdrawal strategy to a Tax-Deferred to Deductions (TDD) approach. Advanced retirement planning software for tax-efficient withdrawal strategies allows you to simulate how your tax bracket changes over time. This is vital for managing:

- Medicare Premiums: Modeling your income to avoid IRMAA (Income-Related Monthly Adjustment Amount) surcharges.

- Required Minimum Distributions (RMDs): Planning Roth conversions today to avoid massive tax bills when you turn 73 or 75.

- Safe Withdrawal Rates (SWR): Determining how much you can draw from different accounts (Taxable, Roth, Traditional) to ensure your money lasts while minimizing the 3.8% Net Investment Income Tax.

By moving your strategy from a spreadsheet to a dedicated modeling tool, you can visualize the long-term impact of these tax decisions, ensuring you don't leave tens of thousands of dollars on the table for the IRS.

FAQ

What features should I look for in retirement planning software?

When evaluating how to choose retirement planning software for diy investors, look for tools that support multi-scenario modeling, tax-aware withdrawal logic, and automated account syncing. High-quality software should offer Monte Carlo simulations to show a range of probabilistic outcomes rather than just a single static line. Additionally, ensure the tool handles specific variables like Social Security optimization and healthcare cost projections.

Can retirement planning software help with tax projections?

Yes, sophisticated retirement planning software is specifically designed to model tax-efficient retirement withdrawals. These tools can help you plan Roth IRA conversion ladders and estimate the impact of Required Minimum Distributions (RMDs). By simulating different tax years, you can identify "tax valleys"—years where your income is low—to strategically move money into tax-free accounts at a lower cost.

Is there any free retirement planning software available?

There is a notable free vs paid diy financial planning software comparison for most investors. Empower offers a highly regarded free dashboard that includes a retirement planner capable of performing thousands of simulations. While free tools are excellent for asset aggregation and basic tracking, paid versions like Boldin or MaxiFi typically offer much deeper customization for complex tax planning and lifestyle smoothing.

What is the difference between professional and consumer retirement software?

Historically, professional software was only available to licensed advisors and offered deeper tax and estate planning modules. However, the current generation of pro-level retirement software for self-directed individual investors has closed that gap. The primary difference now is often the user interface; consumer tools are designed for personal use, while professional tools are built for managing multiple clients simultaneously.

Do I still need a financial advisor if I use retirement planning tools?

While retirement planning software provides the data and projections, a financial advisor can offer behavioral coaching and complex estate planning advice. However, if you are a savvy DIYer, these tools allow you to manage the vast majority of your portfolio strategy independently. Many investors now use software for 90% of their planning and only consult a flat-fee or hourly advisor for a "second opinion" on their digital plan.