Quick Facts

- 2026 Federal Base Rate: 14% applied to the first tier of taxable income.

- RRSP Contribution Limit: A maximum of $32,490 or 18% of prior year's earned income.

- Digital Filing Speed: The Canada Revenue Agency processes 92% of individual returns filed digitally within approximately 2 weeks.

- Paper Filing Delay: Manual returns can take up to 8 weeks for processing compared to electronic methods.

- Filing Deadlines: April 30, 2027, for most individuals; June 15, 2027, for self-employed taxpayers.

- Progressive System: Tax is applied in layers, ensuring a higher income does not result in a lower net take-home pay due to bracket shifts.

Navigating the Canada income tax system often feels like solving a puzzle with moving pieces. With the 2026 federal base rate shifting to 14% and indexation factors changing, understanding your marginal tax rates Canada becomes critical for effective planning. Canada utilizes a progressive Canada income tax system where taxable income is divided into brackets, each taxed at a different marginal rate. For the 2026 tax year, the federal base tax rate is 14% on the first tier of income, with higher percentages applied only to the portions of income that exceed specific thresholds. This means taxpayers do not pay a single high rate on their entire income, but rather a weighted average based on how their earnings are distributed across the 2026 federal and provincial brackets.

Enigma 1: The Bracket Jump Myth and Marginal vs. Average Rates

One of the most persistent anxieties I encounter as an editor is the fear that a salary increase will actually leave you with less money because it "pushes you into a higher bracket." It is a common misconception that once you cross a certain threshold, your entire income is suddenly taxed at that higher percentage. In reality, the Canadian tax brackets explained simply are like a series of buckets.

When you earn money, you fill the first bucket. Once that bucket is full, the excess spills into the second bucket, which is taxed at a slightly higher rate. Crucially, the money staying in the first bucket is still taxed at the lowest rate. This ensures that every extra dollar you earn still results in more money in your pocket, even if the government takes a slightly larger slice of that specific dollar. This distinction is the difference between marginal and average tax rates Canada. Your marginal rate is what you pay on your last dollar earned, while your average rate is the actual percentage of your total income that goes to the Canada Revenue Agency.

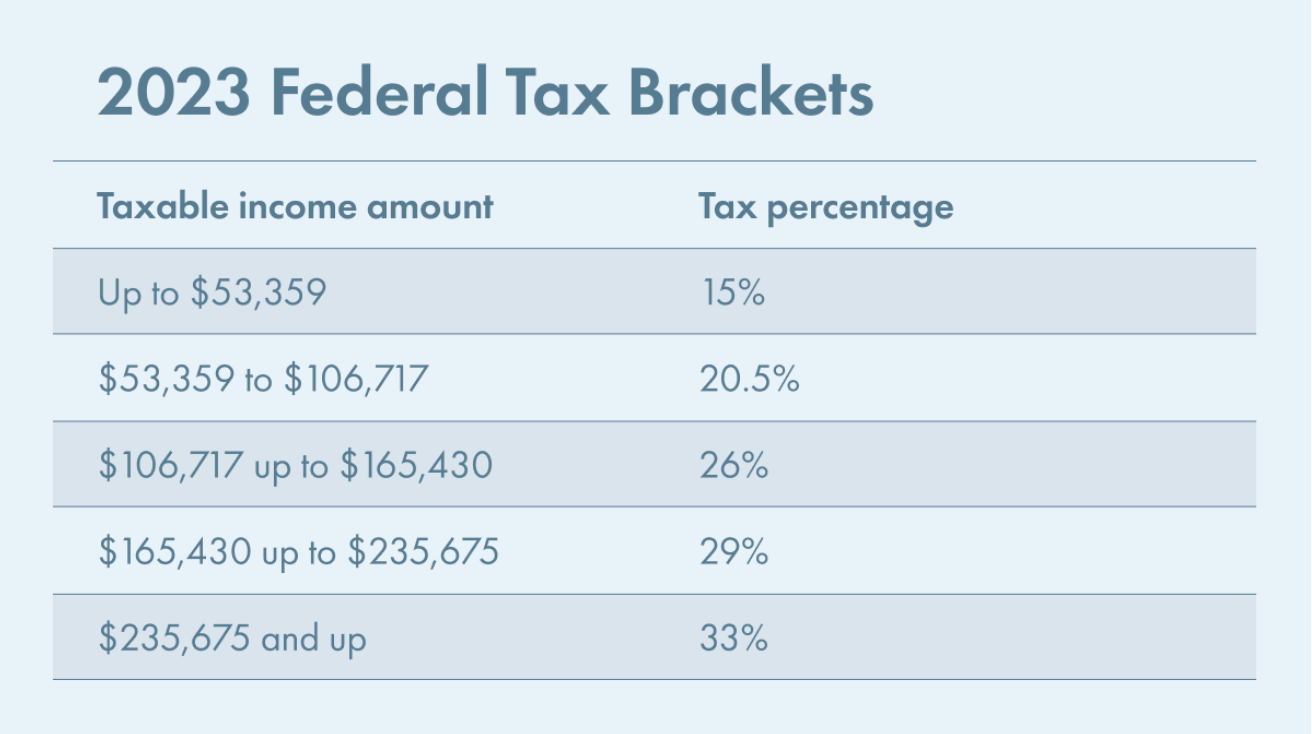

Under the 2026 Canadian federal tax brackets explained in the table below, you can see how these layers stack up. Note that these are federal rates only; provincial taxes are added on top.

| Taxable Income Tier (Estimated for 2026) | Federal Tax Rate |

|---|---|

| First $55,867 | 14% |

| Over $55,867 up to $111,733 | 20.5% |

| Over $111,733 up to $173,205 | 26% |

| Over $173,205 up to $246,752 | 29% |

| Over $246,752 | 33% |

Crunching the Numbers: The Bucket Analogy Imagine you earn $60,000. Under the 2026 rules, the first $55,867 is taxed at 14%. Only the remaining $4,133 is taxed at the 20.5% rate. You do not pay 20.5% on the full $60,000. This is why knowing your marginal tax rates Canada is vital for bonuses or side-hustle planning, but shouldn't scare you away from a promotion.

Enigma 2: Decoding the RRSP Advantage for 2026

If you are looking for the single most effective lever to pull on your tax return, it is the Registered Retirement Savings Plan (RRSP). I often describe the RRSP as a "tax time machine." It allows you to take income earned today—at perhaps your highest career earnings—and defer the tax on it until you retire and are likely in a much lower bracket.

Using an RRSP tax deduction guide is straightforward: any amount you contribute up to your limit is deducted from your gross income. If you earned $90,000 and contributed $10,000 to your RRSP, the government taxes you as if you only earned $80,000. For anyone wondering how RRSP contributions reduce taxable income, the math is immediate and impactful. It can even drop you into a lower marginal bracket entirely, potentially triggering a larger refund.

For the 2026 tax year, the RRSP contribution limit is generally 18% of your 2025 earned income, capped at $32,490. To maximize this, you would need to have earned roughly $180,500 in the previous year. If you haven't maximized your contributions in the past, don't worry. You can find your RRSP unused contribution room on your most recent Notice of Assessment. This "room" carries forward indefinitely, providing a powerful tool for high-income years.

Enigma 3: Federal vs. Provincial – Navigating the Combined Rate

Your total tax bill is never just one number found on a federal chart. Canada requires you to pay both federal and provincial or territorial taxes. While the federal government has introduced the impact of the 2026 federal base tax rate reduction to 14%, each province sets its own specific thresholds. Accurate budgeting for residents or business owners requires calculating combined federal and provincial income tax.

Ontario, for example, uses a "surtax" system which is essentially a tax on the tax you've already calculated. Other provinces, like Alberta, have moved toward indexation via legislation like Bill 32 to ensure that inflation doesn't push residents into higher brackets prematurely. This is why a freelancer in Toronto needs a different savings strategy than a consultant in Calgary, even if they earn the same amount.

The 2026 Ontario combined marginal tax rate guide shows that for mid-to-high earners, the combined impact can exceed 50%. Understanding these figures helps you estimate how much to set aside from every T4 slip or invoice you receive.

| Province | Combined Marginal Rate (at $60k income) | Combined Marginal Rate (at $150k income) |

|---|---|---|

| Ontario | ~29.65% | ~43.41% |

| Alberta | ~24.00% | ~36.00% |

| British Columbia | ~22.70% | ~38.29% |

Enigma 4: Investment Income - Why Not All Dollars Are Equal

It is a mistake to assume the Canada Revenue Agency treats every dollar of profit the same way. The source of your income dictates how it is taxed. Interest earned in a standard savings account is taxed at your full marginal rate, just like salary. However, Capital gains and dividends enjoy special status.

Currently, only 50% of your Capital gains (the profit from selling an asset like a stock or secondary property) are included in your Net income for individuals. This makes them significantly more tax-efficient than interest. Furthermore, there are significant tax benefits of donating publicly traded stocks in Canada. When you donate appreciated stocks directly to a charity, you don't pay any capital gains tax on the increase in value, and you receive a donation receipt for the full market value to use against your taxes.

Dividends from Canadian corporations also receive a "gross-up" and tax credit, which accounts for the fact that the corporation has already paid tax on that profit. This complexity is why the T1 General form has specific schedules just for reporting investment income. If you are serious about wealth building, your portfolio should be structured with these rules in mind.

Enigma 5: The Entrepreneur’s Choice - Salary vs. Dividends

For those engaged in Canadian tax planning for freelancers and self employed, the annual question is usually: Should I pay myself a salary or a dividend from my corporation? This is not just a calculation of the lowest immediate tax; it is a question of long-term compliance and benefits.

A salary is considered earned income, which generates RRSP room and requires you to make CPP contributions. While these contributions "cost" more today, they build a safety net and allow for higher RRSP deductions later. Dividends, on the other hand, are often taxed at a lower personal rate and do not require CPP payments. However, they do not create RRSP room, and lenders (for mortgages or car loans) often view dividend income as less stable than a traditional salary.

I recommend that business owners use modern Tax software to run scenarios for both options. While the federal base rate reduction to 14% helps everyone, the interplay between corporate and personal tax requires a precise touch. Often, a mix of both salary and dividends provides the best balance of immediate cash flow and future retirement security.

FAQ

How is income tax calculated in Canada?

Income tax is calculated using a progressive system where your total taxable income is divided into segments or brackets. Each segment is taxed at its own specific rate. Your total tax is the sum of these segments from both federal and provincial levels, minus any non-refundable credits you are eligible for, such as the basic personal amount.

What are the 2024 Canadian income tax brackets?

For the 2024 tax year, federal brackets started at 15% for the first $55,867 of income. The rates then increased to 20.5%, 26%, 29%, and finally 33% for income over $246,752. These figures are indexed annually for inflation, which is why the 2026 brackets are expected to have slightly higher thresholds and a adjusted base rate of 14%.

What is the deadline for filing income tax in Canada?

For most individuals, the tax filing deadline is April 30 of the following year. If you or your spouse are self-employed, the deadline to file is June 15, although any taxes owed must still be paid by April 30 to avoid interest charges. If April 30 falls on a weekend, the deadline is typically extended to the next business day.

How can I reduce the amount of income tax I pay in Canada?

The most common ways to reduce your tax bill include contributing to an RRSP to lower your taxable income, claiming non-refundable credits like the medical expense tax credit or the Canada training credit, and utilizing tax-free accounts like the TFSA for investments. Business owners can also deduct legitimate business expenses to lower their net income.

What is the difference between federal and provincial taxes?

Federal tax is a consistent set of rates applied to all residents of Canada regardless of where they live. Provincial tax is an additional layer set by each individual province or territory, with its own unique brackets and credits. When you file your personal tax return, these two amounts are combined into a single total tax liability.